Income-driven student loan repayment plans are a lifeline for millions of Americans struggling with educational debt. However, recent updates from the Education Department have caused uncertainty among borrowers. The suspension of certain plans has left many questioning what this means for their financial future and how they should respond.

Understanding these changes is crucial for anyone managing student loans. Borrowers need to stay informed to navigate this complex landscape and ensure they make the best decisions for their financial health. This article delves into the details of the suspension, its implications, and actionable steps borrowers can take.

By the end of this article, you'll have a comprehensive understanding of the situation and be equipped with the tools to manage your student loans effectively. Whether you're directly affected or simply want to stay informed, this guide is for you.

Read also:Unlocking The Secrets Of Archivebate A Comprehensive Guide

Table of Contents

- Overview of Income-Driven Repayment Plans

- Why the Education Department Suspended Certain Plans

- Who Is Affected by the Suspension?

- Eligibility for Income-Driven Repayment Plans

- Implications of the Suspension

- Steps Borrowers Should Take

- Alternative Repayment Options

- Resources for Borrowers

- What the Future Holds for Student Loan Repayment

- Conclusion and Call to Action

Overview of Income-Driven Repayment Plans

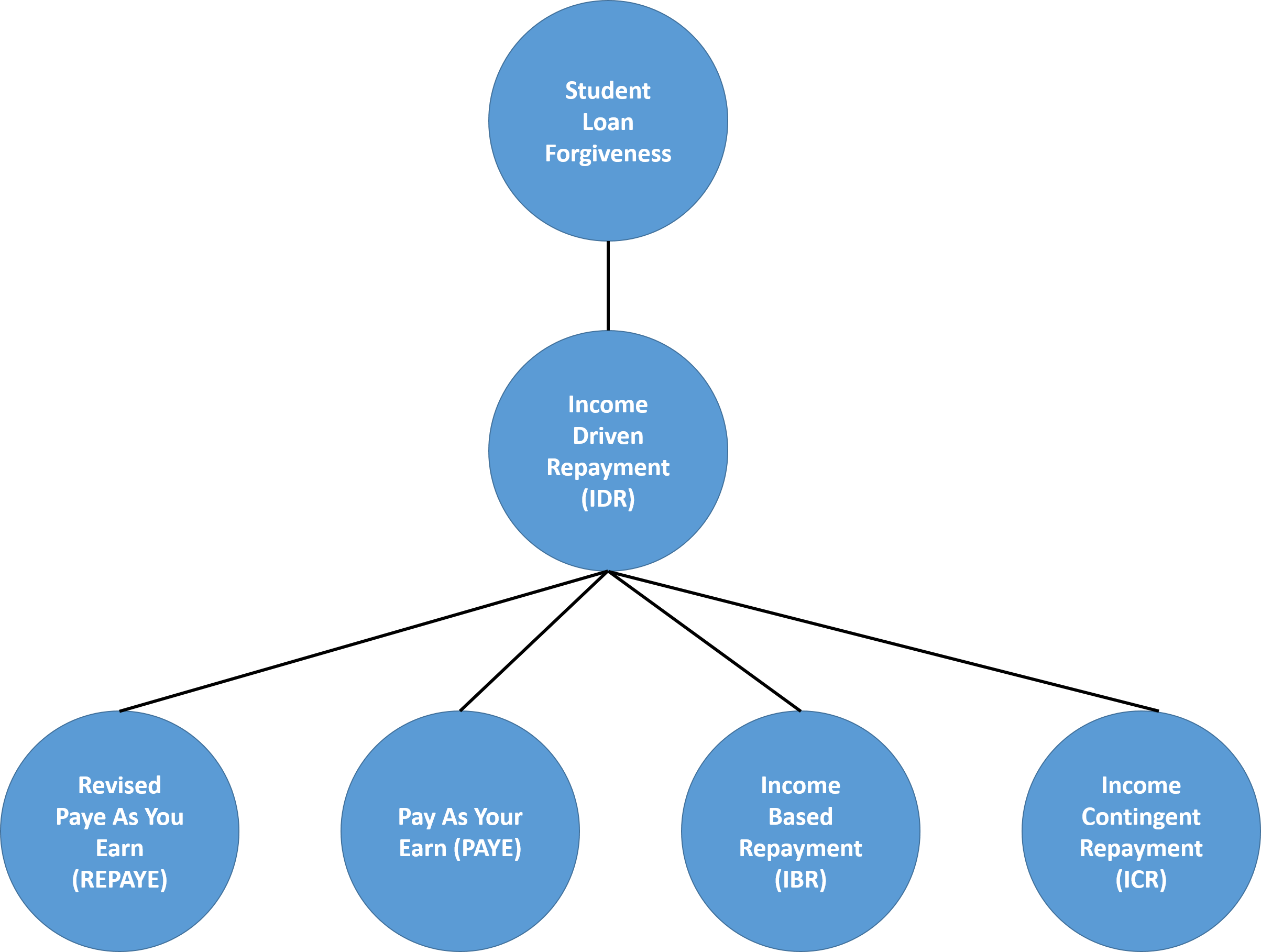

Income-driven repayment (IDR) plans are designed to make student loan repayment more manageable by capping monthly payments based on a borrower's income and family size. These plans are particularly beneficial for individuals with high loan balances relative to their earnings. The four main IDR plans include:

- Income-Based Repayment (IBR)

- Pay As You Earn (PAYE)

- Revised Pay As You Earn (REPAYE)

- Income-Contingent Repayment (ICR)

Each plan has its own eligibility criteria and repayment terms. Borrowers can typically expect to pay between 10% and 20% of their discretionary income each month. After a set period (usually 20 or 25 years), any remaining balance may be forgiven.

How Income-Driven Repayment Works

Under IDR plans, borrowers submit annual income documentation to their loan servicer. Based on this information, the servicer recalculates the monthly payment amount. This ensures that payments remain affordable as the borrower's financial situation changes over time.

For example, a borrower earning $30,000 annually with a family size of one might have a monthly payment of around $150 under PAYE. If their income increases to $50,000, the payment would adjust accordingly to reflect the higher earnings.

Why the Education Department Suspended Certain Plans

The Education Department's decision to suspend certain income-driven repayment plans stems from a broader review of the student loan system. Officials aim to address inefficiencies, streamline processes, and ensure fairness across all repayment options. In some cases, the suspension is temporary while the department evaluates specific aspects of the programs.

One reason for the suspension is the complexity of administering multiple IDR plans. With overlapping features and varying rules, borrowers often face confusion when selecting the most suitable option. By pausing certain plans, the department hopes to simplify the system and improve borrower outcomes.

Read also:Sofiacutea Vergaras Husband A Comprehensive Look At Her Love Life And Relationship

Key Factors Behind the Decision

Several factors contributed to the suspension:

- Administrative challenges in managing multiple IDR plans

- Disparities in benefits across different repayment options

- Concerns about borrower understanding and program accessibility

Who Is Affected by the Suspension?

The suspension primarily impacts borrowers who were considering enrolling in or switching to the affected IDR plans. While existing participants in these plans are generally unaffected, new applicants may find their options limited. Borrowers should verify their eligibility and explore alternative solutions if necessary.

For instance, individuals who were planning to switch from standard repayment to PAYE or REPAYE may need to reconsider their strategy. Those already enrolled in these plans will continue to benefit from the terms they agreed to upon enrollment.

Assessing Your Situation

To determine whether you're affected by the suspension, consider the following:

- Your current repayment plan

- Your income level and expected changes

- Your loan balance and type

Borrowers with federal Direct Loans or Federal Family Education Loans (FFEL) are most likely to be impacted by these changes.

Eligibility for Income-Driven Repayment Plans

Eligibility for IDR plans depends on several factors, including the type of loan, the borrower's income, and their family size. Federal Direct Loans and FFELs are typically eligible, while private loans are not. Borrowers must also demonstrate financial need by showing that their monthly payments under a standard repayment plan exceed a certain percentage of their discretionary income.

For example, a borrower with a Direct Subsidized Loan earning $40,000 annually and supporting a family of three would likely qualify for an IDR plan. On the other hand, someone with a high income relative to their debt burden might not meet the eligibility criteria.

Steps to Verify Eligibility

To confirm your eligibility for an IDR plan:

- Review your loan type and servicer

- Calculate your discretionary income

- Compare your potential monthly payment under IDR to the standard plan

Using an online calculator or consulting with your loan servicer can simplify this process.

Implications of the Suspension

The suspension of certain IDR plans has both short-term and long-term implications for borrowers. In the immediate future, some individuals may face delays in accessing affordable repayment options. Over time, the Education Department's efforts to streamline the system could lead to improved program design and better borrower outcomes.

However, borrowers must remain vigilant and proactive in managing their loans during this transition period. Staying informed about updates and alternative solutions is essential to maintaining financial stability.

Short-Term vs. Long-Term Effects

Short-term effects include:

- Limited access to specific IDR plans

- Potential confusion among borrowers

Long-term effects may involve:

- Streamlined program offerings

- Enhanced borrower support and resources

Steps Borrowers Should Take

In light of the suspension, borrowers should take proactive steps to manage their student loans effectively. First, review your current repayment plan and assess whether it meets your financial needs. If you're considering switching to an IDR plan, explore alternative options and gather all necessary documentation.

Additionally, stay informed about updates from the Education Department and your loan servicer. Regularly check official websites and sign up for alerts to ensure you receive the latest information.

Actionable Tips for Borrowers

Here are some practical steps to take:

- Contact your loan servicer for guidance

- Explore alternative repayment plans

- Consider loan consolidation if applicable

By taking these steps, you can minimize the impact of the suspension on your financial well-being.

Alternative Repayment Options

While certain IDR plans are suspended, borrowers have access to several alternative repayment options. Standard repayment plans, graduated repayment plans, and extended repayment plans offer varying terms to suit different financial situations. Additionally, loan consolidation can simplify payments and potentially lower interest rates.

For example, a borrower with multiple loans might benefit from consolidating them into a single Direct Consolidation Loan. This approach can streamline repayment and provide access to additional IDR options.

Evaluating Alternatives

When evaluating alternative repayment options, consider the following:

- Monthly payment amounts

- Interest rates and total repayment costs

- Eligibility requirements

Consulting with a financial advisor or loan counselor can help you make an informed decision.

Resources for Borrowers

Borrowers have access to numerous resources to assist them in navigating the complexities of student loan repayment. The Federal Student Aid website provides comprehensive information on IDR plans, eligibility criteria, and application processes. Additionally, nonprofit organizations and private companies offer counseling services to help borrowers manage their debt.

For example, borrowers can use the Repayment Estimator tool on the Federal Student Aid website to compare repayment options and estimate monthly payments. This resource can be invaluable in making informed decisions about loan management.

Recommended Resources

- Federal Student Aid: studentaid.gov

- Consumer Financial Protection Bureau: www.consumerfinance.gov

- Student Loan Borrower Assistance: www.studentloanborrowerassistance.org

What the Future Holds for Student Loan Repayment

The future of student loan repayment is likely to involve continued evolution and refinement of existing programs. As the Education Department works to address inefficiencies and improve borrower outcomes, we can expect to see changes in the structure and administration of IDR plans. Borrowers should remain adaptable and open to exploring new options as they become available.

In the long term, these efforts may lead to a more equitable and accessible student loan system. By staying informed and engaged, borrowers can navigate these changes with confidence and achieve financial stability.

Predictions for the Future

Some potential developments include:

- Consolidation of IDR plans into a single option

- Enhanced borrower support and resources

- Increased emphasis on loan forgiveness programs

Conclusion and Call to Action

In conclusion, the suspension of certain income-driven repayment plans by the Education Department highlights the ongoing need for borrowers to stay informed and proactive in managing their student loans. By understanding the implications of these changes and exploring alternative solutions, you can ensure a stable financial future.

We encourage you to take action by reviewing your repayment options, consulting with experts, and utilizing available resources. Share this article with others who may benefit from the information, and don't hesitate to leave a comment or question below. Together, we can navigate the complexities of student loan repayment and achieve financial success.